Portfolio Standard Deviation Calculator

Calculate portfolio risk with asset weights, standard deviations, and correlations

| Asset | Weight (%) | Std Dev (%) | Action |

|---|---|---|---|

| Asset 1 | |||

| Asset 2 | |||

| Asset 3 |

Portfolio Risk Comparison

Step-by-Step Solution

Assets in the portfolio:

| Asset | Weight (w) | Std Dev (σ) |

|---|---|---|

| Asset 1 | 40% | 15% |

| Asset 2 | 35% | 20% |

| Asset 3 | 25% | 10% |

Correlations between assets:

| Asset 1 | Asset 2 | Asset 3 | |

|---|---|---|---|

| Asset 1 | 1.00 | 0.50 | 0.30 |

| Asset 2 | 0.50 | 1.00 | 0.40 |

| Asset 3 | 0.30 | 0.40 | 1.00 |

Portfolio variance is calculated as:

σp2 = ∑∑ wi wj σi σj ρij

Where w is weight, σ is standard deviation, and ρ is correlation coefficient.

Calculating each component:

σp2 = (0.4×0.4×0.15×0.15×1) + (0.4×0.35×0.15×0.2×0.5) + … = 0.0153

Portfolio Variance: 0.0153

Standard Deviation = √Variance

σp = √0.0153 ≈ 0.1235 or 12.35%

Portfolio Standard Deviation: 12.35%

In an era of accelerated market complexity and broadening investment access, tools that measure and manage risk are essential. The Portfolio Standard Deviation Calculator is one such indispensable instrument. Whether you are a retail investor trying to balance a retirement account, a financial advisor constructing diversified portfolios, a state official designing pension fund policy, or an NGO working on financial inclusion, understanding how to calculate and interpret portfolio volatility is critical. This article provides a thorough, detailed, and practical exploration of the Portfolio Standard Deviation Calculator, covering its history, methodology, objectives, regional and state-level impacts, implementation strategies, success stories, limitations, comparisons with alternative risk measures, and future prospects — plus a targeted FAQs section to clarify common questions.

Introduction to Portfolio Risk and the Role of the Portfolio Standard Deviation Calculator

Risk is the language of finance. Measuring risk is the prerequisite for managing it. The Portfolio Standard Deviation Calculator quantifies the dispersion of portfolio returns around their mean and provides investors a single, digestible measure of volatility. Unlike tools that merely track price or return trends, a robust Deviation Calculator integrates asset weights, individual volatilities, and cross-asset correlations — converting a portfolio’s complexity into actionable insight.

Widespread adoption of the Portfolio Standard Deviation Calculator is driven by three factors: (1) the democratization of financial data and calculators through web and mobile apps; (2) policy frameworks that emphasize prudent fund management at the state and institutional level; and (3) grassroots financial literacy programs focused on rural development and women empowerment schemes that encourage risk-aware investment.

Historical Origins: From Variance to Modern Portfolios

The intellectual foundation of the Deviation Calculator stems from early 20th-century statistics and mid-century finance theory. Variance and standard deviation have long been statistical cornerstones; their financial application was formally articulated in Harry Markowitz’s Modern Portfolio Theory (MPT) in the 1950s. Markowitz demonstrated that investors should consider not only expected returns but also the covariance among assets when constructing efficient portfolios.

The Portfolio Standard Deviation Calculator operationalizes Markowitz’s insight. Where once portfolio managers computed variance manually, today’s calculators enable rapid stress testing and exploration of “what-if” scenarios across thousands of asset combinations. As financial markets globalized, the need for standardized, replicable risk metrics — embodied by the Deviation Calculator — became essential for regulators, fund managers, and individual investors.

What Exactly Is the Portfolio Standard Deviation Calculator?

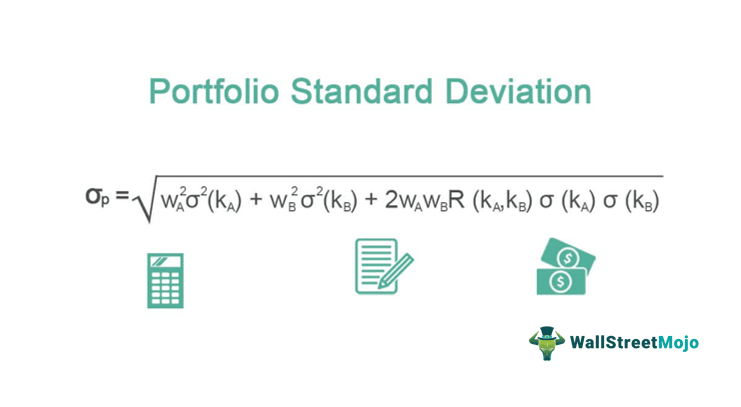

At its core, a Portfolio Standard Deviation Calculator computes the square root of the portfolio variance. The basic formula for a two-asset portfolio generalizes to an n-asset portfolio:

Portfolio variance = Σᵢ Σⱼ wᵢ wⱼ Cov(Rᵢ, Rⱼ)

Portfolio standard deviation = √(Portfolio variance)

Where:

- wᵢ = weight of asset i in the portfolio

- Cov(Rᵢ, Rⱼ) = covariance between returns of assets i and j

A practical Portfolio Standard Deviation Calculator accepts inputs such as historical returns, asset weights, or expected standard deviations and correlation matrices. It then outputs a single figure — the portfolio standard deviation — and often complementary metrics (e.g., variance decomposition, marginal contribution to risk).

This output lets investors compare portfolios on a risk-adjusted basis. Many platforms augment the Calculator with sensitivity analysis, enabling users to see how changing an asset’s weight or its correlation affects total portfolio volatility.

Objectives: Why Use a Portfolio Standard Deviation Calculator?

1. Quantify and Communicate Risk

The Portfolio Standard Deviation Calculator translates multifaceted volatility data into one interpretable number. For boards, clients, and stakeholders, this clarity aids communication and informed decision-making.

2. Support Diversification and Optimization

By making the role of correlation explicit, a Portfolio Standard Deviation Calculator Calculator shows how combining assets reduces risk. It provides an empirical basis for rebalancing and constructing efficient frontiers.

3. Inform Policy and State-Level Fund Management

Pension funds, sovereign wealth funds, and other public vehicles benefit from the Portfolio Standard Deviation Calculator when implementing liability-driven investing and fulfilling fiduciary responsibilities under the state policy framework.

4. Empower Financial Inclusion and Rural Development

When embedded in community financial literacy curricula, the Portfolio Standard Deviation Calculator demystifies risk for small-scale savers, women entrepreneurs, and rural development cooperatives seeking low-volatility investment strategies.

How to Use a Portfolio Standard Deviation Calculator Calculator: A Practical Walkthrough

A modern Portfolio Standard Deviation Calculator typically follows these steps:

- Choose the data horizon: Select daily, weekly, or monthly returns. Longer horizons reduce noise but may miss short-term regime shifts.

- Input asset weights: Manual entry or automated import from brokerage accounts.

- Provide individual asset volatilities: These can be historical standard deviations or model-based estimates.

- Supply a correlation or covariance matrix: This is the most critical input. Poor correlation estimates distort the Calculator’s output.

- Run the calculation: The tool computes portfolio variance and returns √(variance) as the portfolio standard deviation.

- Interpret and iterate: Use sensitivity checks — e.g., change weights, substitute assets, or alter correlation assumptions — to understand risk drivers.

Some Portfolio Standard Deviation Calculator implementations also include Monte Carlo simulations, allowing users to model extreme events and distributional deviations that a single standard deviation number may obscure.

Implementation: From Excel to Cloud Platforms

The Calculator exists in many forms:

- Spreadsheet templates: Popular with advisors and students; they illustrate formula mechanics and are highly transparent.

- Dedicated web calculators: Consumer-facing, often free, with friendly UIs that automatically fetch market data.

- Brokerage dashboards and robo-advisors: Integrated into investment platforms where the Portfolio Standard Deviation Calculator informs algorithmic allocation and rebalancing rules.

- Institutional risk systems: Enterprise-grade Portfolio Standard Deviation Calculators tie into risk control, regulatory reporting, and enterprise data warehouses.

Adoption depends on user sophistication: spreadsheets provide educational value, while cloud systems scale to millions of accounts and deliver real-time recalculations.

Data Quality and the Limits of the Portfolio Standard Deviation Calculator

The Portfolio Standard Deviation Calculator is only as reliable as its inputs. Common pitfalls include:

- Overreliance on historical data: Past volatility is not always a reliable predictor of future risk, especially around structural regime changes.

- Incorrect correlation estimates: During market stress, correlations often converge to 1.0, undermining diversification benefits a Portfolio Standard Deviation Calculator might otherwise suggest.

- Ignoring tail risk: Standard deviation captures dispersion under the assumption of symmetric distributions; it underestimates extreme downside risk if returns exhibit skewness or kurtosis.

- Operational errors: Mistakes in data frequency alignment, currency conversion, or weight normalization can produce misleading Calculator outputs.

Prudent users treat the Calculator as a starting point rather than the only decision input, supplementing it with stress tests, VaR, scenario analysis, and qualitative risk assessment.

Regional Impact: How the Portfolio Standard Deviation Calculator Drives Local Change

The Portfolio Standard Deviation Calculator has proven utility across diverse economic contexts:

Developed Markets

In advanced financial centers, institutional investors embed the Portfolio Standard Deviation Calculator in systematic portfolio construction and regulatory capital assessments. State pension funds use it to align asset allocation with liabilities under a rigorous policy framework.

Emerging Markets

For emerging economies, the Portfolio Standard Deviation Calculator supports sovereign wealth funds, development finance institutions, and regional banks in balancing growth objectives with volatility control. It helps public managers design investment guidelines that reflect currency risk, political risk, and market liquidity constraints.

Rural and Community Finance

At the grassroots, simplified Portfolio Standard Deviation Calculator tools integrated into microfinance trainings and cooperative accounting software help community treasurers understand how to diversify short-term reserves and emergency funds, reinforcing rural development goals.

Women Empowerment Schemes

Digital financial literacy initiatives for women often include step-by-step modules on how to use a Portfolio Standard Deviation Calculator. By quantifying risk, these programs encourage women entrepreneurs and savers to shift some capital into low-volatility instruments, improving financial resilience and enabling entrepreneurial growth.

State-Level Policy Frameworks and Benefits

States and provinces can leverage the Portfolio Standard Deviation Calculator within broader financial policy in five ways:

- Pension Management: Mandating risk assessment using a Portfolio Standard Deviation Calculator helps stabilize long-term liabilities and aligns investment policy statements with acceptable volatility thresholds.

- Public Investment Oversight: Auditors and legislators can require periodic Portfolio Standard Deviation Calculator reports for quasi-public funds and infrastructure SPVs.

- Education and Inclusion: Integrating the Calculator into school and community curricula supports informed saving behavior, contributing to state-wide financial health.

- Regulatory Guidance for Microfinance: A Calculator can be a recommended element in the operational manuals of microfinance institutions to reduce portfolio risk and protect depositors.

- State Grants and Matching Funds: Programs that disburse matching investment capital to local cooperatives can condition grants on risk assessments produced by a Portfolio Standard Deviation Calculator to ensure prudent use of funds.

These state-wise benefits create stronger fiscal resilience, better outcomes for social welfare initiatives, and improved trust in public financial management.

Success Stories: Real-World Applications of the Portfolio Standard Deviation Calculator

Several real examples illustrate the Calculator’s impact:

- Municipal Pension Reform: A mid-sized city introduced mandatory Portfolio Standard Deviation Calculator reporting for its pension committee. By shifting toward lower-correlation assets and rebalancing more systematically, the pension plan reduced expected volatility and improved funded status resilience during a market downturn.

- Cooperative Savings in Southeast Asia: Agricultural cooperatives used a mobile Portfolio Standard Deviation Calculator application to design reserve funds. The tool encouraged diversification into short-term government securities and diversified credit instruments, reducing community losses after a drought-related shock.

- Women’s Entrepreneurship Program in East Africa: NGOs taught small groups to use a simplified Calculator. Entrepreneurs who diversified cash reserves away from single suppliers experienced improved continuity of business operations, which strengthened livelihoods and increased reinvestment rates.

- State Infrastructure Fund: A state development bank incorporated a Portfolio Standard Deviation Calculator into its project finance assessment. The bank used the results to price guarantees and set aside contingency buffers tied to expected portfolio volatility.

These stories underscore the Portfolio Standard Deviation Calculator’s value beyond theory — as a practical instrument that contributes to financial stability and social welfare initiatives.

Challenges and Criticisms

Critics of an overemphasis on the Portfolio Standard Deviation Calculator point out:

- False Precision: Presenting a single volatility number can give a misleading sense of certainty. A Portfolio Standard Deviation Calculator may not reflect tail events or liquidity squeezes.

- Model Risk: Inaccurate assumptions (normality of returns, stable correlations) can produce deceptive outputs. Users must consider model risk and validate assumptions.

- Accessibility Barriers: Despite mobile penetration, there remains a digital divide. Many rural areas lack the infrastructure to use sophisticated Portfolio Standard Deviation Calculator apps without support.

- Cultural Resistance: In some communities, financial decisions emphasize social factors over quantitative analysis. Adoption of the Portfolio Standard Deviation Calculator requires sensitive community engagement.

Addressing these challenges involves strengthening data governance, pairing calculators with educational programs, and complementing standard deviation outputs with narrative scenario analysis.

Comparing the Portfolio Standard Deviation Calculator with Other Risk Metrics

The Portfolio Standard Deviation Calculator is one of many tools in a risk manager’s toolbox. Comparative context:

- Value at Risk (VaR): VaR estimates the maximum expected loss at a given confidence level. The Portfolio Standard Deviation Calculator gives overall dispersion, while VaR focuses on near-worst-case outcomes. Both are useful; using them together is common practice.

- Conditional VaR (CVaR): CVaR (or expected shortfall) measures average losses beyond the VaR threshold. When tail risk is important, CVaR complements the Portfolio Standard Deviation Calculator.

- Sharpe Ratio: The Sharpe ratio uses the portfolio standard deviation in its denominator to express risk-adjusted returns. The Portfolio Standard Deviation Calculator thus directly feeds into performance metrics.

- Beta: Beta measures systematic risk relative to a market benchmark. The Portfolio Standard Deviation Calculator measures total portfolio volatility, including idiosyncratic risk.

- Stress Testing and Scenario Analysis: These methods simulate specific events (currency crises, sudden rate hikes) that a Portfolio Standard Deviation Calculator may not capture in isolation. Integrating stress tests provides a fuller picture.

In practice, the Portfolio Standard Deviation Calculator is most powerful when used alongside these complementary metrics; it is rarely the sole basis for high-stakes decisions.

Building Trust: Best Practices for Deploying a Portfolio Standard Deviation Calculator

To achieve reliable and actionable results from a Portfolio Standard Deviation Calculator, adopt these best practices:

- Use Stable, High-Quality Data: Prefer longer return histories where appropriate, but adjust for structural breaks.

- Harmonize Frequencies: Ensure uniform return frequency (e.g., monthly for all assets) before calculating covariance.

- Regularly Update Correlations: Use rolling windows and stress scenarios to capture correlation dynamics.

- Communicate Assumptions: Every Portfolio Standard Deviation Calculator output should be accompanied by clear assumptions about data horizon, treatment of outliers, and underlying distributional assumptions.

- Pair Quantitative Outputs with Qualitative Insight: Consider liquidity, regulatory changes, and political risk, especially in the context of regional development and state projects.

- Train End Users: Educational modules — tailored for women empowerment schemes, rural cooperatives, and municipal committees — improve interpretation and adherence to risk limits.

Adhering to these practices increases the credibility and practical utility of the Portfolio Standard Deviation Calculator.

Future Prospects: AI, ESG, and Democratization of Risk Tools

The future of the Portfolio Standard Deviation Calculator looks promising and will likely evolve in several directions:

AI and Machine Learning Integration

Advanced models can improve volatility and correlation estimates by ingesting higher-frequency data, alternative datasets (satellite, transaction flows), and non-linear relationships. AI enhancements will allow a Portfolio Standard Deviation Calculator to better detect structural changes and regimes.

Incorporation of ESG and Sustainability Factors

As Environmental, Social, and Governance (ESG) considerations drive capital allocation, Portfolio Standard Deviation Calculator implementations will incorporate ESG-linked factor volatilities and correlations, aligning investment risk analysis with long-term sustainability objectives.

Mobile and Localized Tools for Inclusion

Low-bandwidth, language-localized Portfolio Standard Deviation Calculator apps will expand access in underserved regions. Tying calculators to state financial literacy programs, social welfare initiatives, and women empowerment schemes will democratize risk understanding.

Regulatory Adoption and Standardization

As regulators demand improved risk reporting, the Portfolio Standard Deviation Calculator — standardized and auditable — may become a required disclosure for certain public funds and financial intermediaries, underpinning a stronger policy framework for fiscal prudence.

A Roadmap for Institutions and Communities

To harness the Portfolio Standard Deviation Calculator effectively at scale, stakeholders should consider the following roadmap:

- Assessment Phase: Inventory current tools and identify data gaps.

- Pilot Deployments: Test a simple Portfolio Standard Deviation Calculator with a few cooperative groups, a municipal pension subaccount, or a women entrepreneur cohort.

- Training and Capacity Building: Run workshops tailored to local languages and contexts, emphasizing interpretation and practical steps.

- Integration with Policy: Embed the Portfolio Standard Deviation Calculator outputs in investment policy statements, microfinance guidelines, and grant evaluation frameworks.

- Monitoring and Evaluation: Use quantifiable metrics — change in portfolio volatility, default rates, and participant satisfaction — to evaluate impact.

- Scale and Institutionalize: Scale the tool with cloud infrastructure, open APIs, and partnerships across state agencies and NGOs.

This approach ensures the Portfolio Standard Deviation Calculator is not a stand-alone product but an integrated component of a broader financial inclusion and governance ecosystem.

Conclusion: The Portfolio Standard Deviation Calculator as a Bridge Between Theory and Impact

The Portfolio Standard Deviation Calculator distills a complex statistical concept into a practical instrument for decision-making — spanning retail investors, institutional managers, state agencies, and community organizations. Its capacity to inform diversification, support policy frameworks, and assist state-wise benefits programs makes it a valuable addition to any financial toolkit.

Yet, the tool’s true value emerges when combined with education, thoughtful implementation, and complementary risk measures. When introduced as part of women empowerment schemes, rural development programs, and social welfare initiatives, the Portfolio Standard Deviation Calculator can help transform abstract risk into manageable concepts that protect savings, strengthen institutions, and foster resilient communities.